Published:

Amenity Trends in London’s New-Build Developments: What the Data Shows

Amenities have moved from optional extras to strategic tools in London’s new-build residential market. This analysis draws on data from 166 private sale London developments completed / completing between 2020 and 2026, offering a clear view of the amenity provision across new build developments in London. This analysis excludes shared ownership schemes, PRS and social housing developments.

This reveals clear trends around which features have become standard, which remain premium and emerging offerings. For developers, investors and buyers alike, these patterns are increasingly important in a market defined by higher density, smaller private spaces, and greater competition.

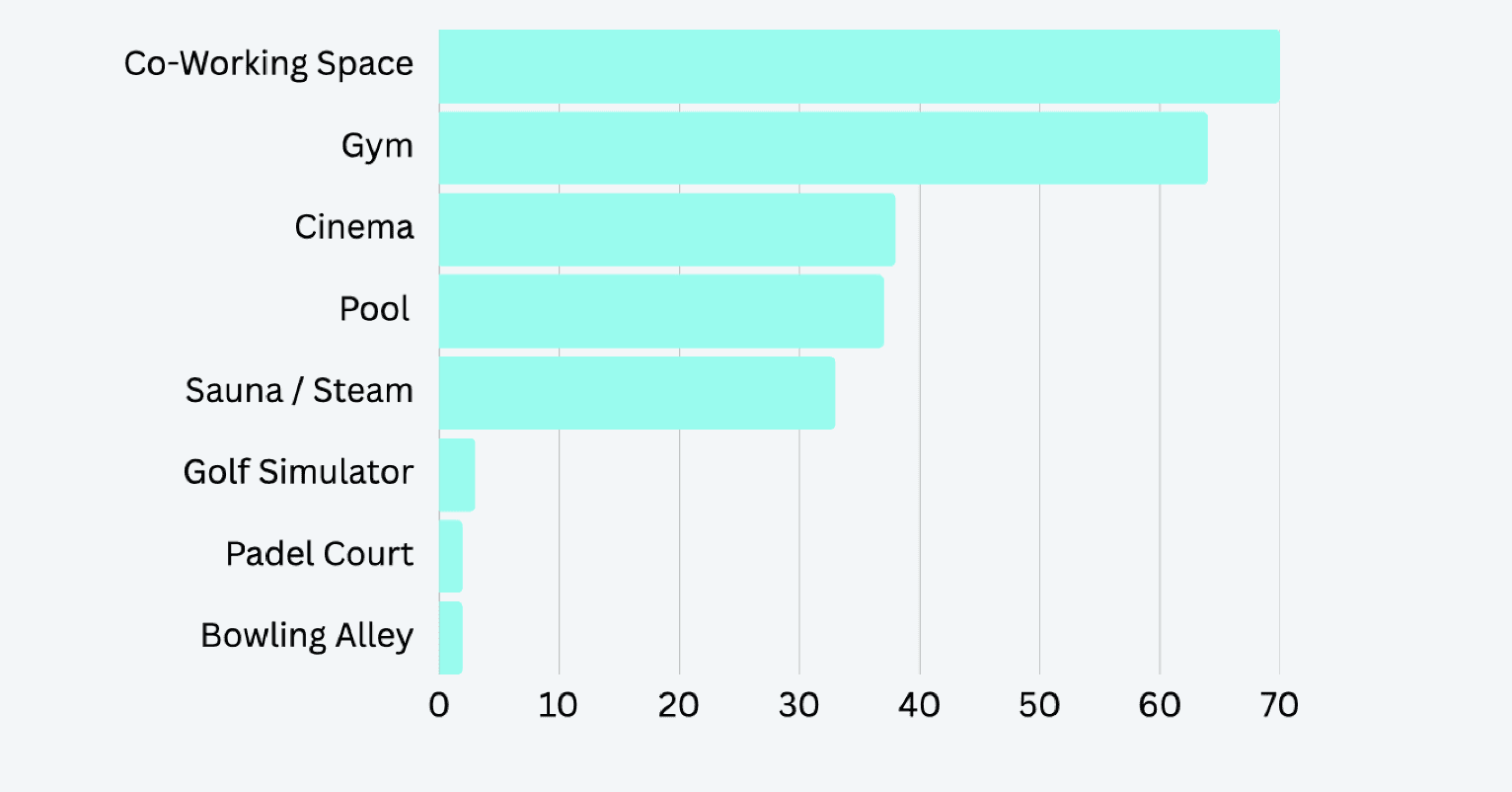

The percentage of developments with each amenity offering.

Why Are Amenities So Important in London’s New-Build Developments?

Amenities play an increasingly central role in buyer decision-making, particularly in a market where many developments share similar layouts, specifications, and locations. As apartment sizes in London have reduced over time, private living space has become more constrained, making the quality of shared spaces far more important to day-to-day livability.

Amenities play different strategic roles depending on location. In premium areas of London, strong amenity provision helps developments stand out, justify higher prices and meet the expectations of wealthier purchasers. In weaker markets, amenities serve a different purpose, helping to improve liveability and encouraging buyers to move into emerging areas. In both cases, amenities act as a key tool for attracting demand where competition or location alone is not enough.

Larger, well-designed communal areas help offset smaller private apartments by giving residents access to places to work, exercise, socialise and relax beyond their front door. In dense urban schemes, these shared amenities effectively extend the living space of each home, making apartments easier and more comfortable to live in without increasing unit size.

Since 2020, this shift has accelerated. Remote and hybrid working, a stronger focus on health and wellbeing and rising buyer expectations have all pushed amenities from “nice to have” into the category of baseline infrastructure. For developers, amenity provision now directly influences absorption rates, achievable sales pricing, sensitivity to service charges and the long-term reputation of a building.

Which Amenities Are Most Common in London’s New-Build Developments?

The data reveals a clear hierarchy of amenities across London developments. Co-working spaces are now the most common amenity, followed closely by gyms, which appear in the majority of schemes. Pools, private cinemas, and wellness facilities are far less common and remain concentrated in a smaller segment of the market.

The widespread adoption of co-working spaces since Covid reflects how developments have adapted to new living patterns. At the same time, the growing focus on health and wellbeing has reshaped gym provision. Developers are increasingly delivering high-quality, fully equipped gyms rather than the small fitness rooms with limited equipment that were common prior to 2020. Swimming pools, while still present, tend to appear in higher-end developments or large-scale schemes where their cost can be spread across a greater number of units and aligned with a more premium positioning.

Why Are Co-Working Spaces the Leading Amenity Trend?

Co-working spaces now appear in approximately 70 percent of the new-build developments analysed, making them the most prevalent amenity in London schemes. This reflects a structural lifestyle change rather than a temporary response to the pandemic.

As working from home has become embedded in daily life, residents increasingly need dedicated space beyond their apartment to focus, collaborate, or take calls. From a development perspective, co-working spaces are attractive because they require relatively little specialist infrastructure, optimise ground floor space and deliver high perceived value.

Are Gyms Now a Standard Feature in London New-Builds?

Private gyms now appear in roughly two-thirds of new London developments, placing them firmly in the “expected” category rather than the “luxury” tier. However, the nature of these gyms has changed significantly.

Newer developments increasingly feature well-designed, modern gyms with a broad range of equipment rather than minimal fitness rooms. This trend aligns closely with the demographics of many new-build schemes, which are often occupied by younger working professionals with a growing interest in health and wellbeing,. For these buyers and renters, a gym is no longer an occasional convenience but part of their everyday routine, making it a key driver of sales and rental demand.

At the same time, the wider London fitness market has evolved. The growth of premium gyms such as Third Space has raised expectations around quality, design, and equipment expected. As a result, in-building gyms need to meet a higher standard to remain a key amenity.

Why are Pools not More Prevalent in London New Build Developments?

Swimming pools appear in around one-third of developments and their prevalence has largely plateaued. Despite their continued marketing appeal, these amenities are expensive to build, operate and take up large amounts of space.

Pools significantly increase service charges and are difficult to justify in smaller schemes. As a result, they are typically reserved for high-density developments and prime central locations where expectations of luxury are higher and price sensitivity is lower.

Is Wellness Still a Growing Amenity Trend?

Wellness amenities such as saunas and steam rooms appear in roughly 30 percent of developments, most often integrated alongside gym facilities rather than delivered as standalone spaces. The emphasis has shifted away from scale and toward efficiency.

Developers are favouring compact wellness features that complement existing amenities and are easier to manage operationally. At the same time, interest in wellness continues to evolve. Saunas and cold plunges have grown in popularity and can influence purchasing decisions, particularly among health-conscious buyers. However, these features come with high upfront and ongoing costs, meaning their inclusion must be carefully balanced against long-term affordability.

Should Developments Include More Niche Amenities?

Niche amenities such as golf simulators, padel courts, and bowling alleys appear in fewer than 5 percent of developments. While they can offer differentiation, they remain difficult to justify in most apartment-led schemes.

Padel’s rapid rise in popularity has renewed interest in sports-led amenities, but space constraints in residential developments often limit feasibility. Golf simulators, which require less space, are becoming more popular as a flexible option, but their appeal remains concentrated among specific buyer groups. For most developments, niche amenities remain a higher-risk strategy rather than a reliable driver of value.

How Do Amenities Impact Service Charges in New-Build Developments?

As amenity provision expands, service charge sensitivity has become a more prominent factor in buyer decision-making. Purchasers are increasingly assessing not just the presence of amenities, but their ongoing cost and value for money. Larger or premium developments are better positioned to absorb amenity costs, making premium facilities more viable. Smaller developments face a tighter balance.

In an environment of higher interest rates and increased financial pressure due to higher interest rates, buyers are becoming increasingly aware of high service charges when looking at purchasing a property.

What Do These Amenity Trends Mean for Future London Developments?

The data points toward a clear direction for future schemes. Co-working spaces and gyms have become baseline expectations rather than true differentiators, meaning their absence is far more noticeable than their presence. At the same time, buyers are increasingly price-sensitive, making high operating-cost amenities harder to justify unless they clearly align with the target market and deliver real, ongoing value.

Location also plays a growing role in amenity strategy. Developments within emerging areas of London increasingly rely on strong amenity provision to remain competitive and to justify encouraging buyers to move further from established centres. Conversely, in high-end, prime developments, comprehensive amenity offerings are no longer optional. These schemes are expected to include the full suite of premium amenities, making differentiation more difficult and shifting competition toward quality, execution, and long-term management.